This time last year we published an article on the Help to Buy scheme and how the mortgage side of the process works. With the scheme becoming ever more popular, and confirmation from the Government the scheme will remain in place until at least 2023, we have refreshed our original article and updated it to reflect some refinements to the scheme.

Greg Cunnington, director of lender relationships and new homes at Alexander Hall, discloses how using an intermediary has helped first-time buyers to navigate the Help to Buy scheme and successfully get onto the property ladder.

The government’s hugely successful Help to Buy scheme was launched in April 2013, with Help to Buy London following in February 2016. Since its inception, over 180,000 properties have been purchased with a combined value of over £46.5 billion!

Last year’s Autumn budget revealed that the scheme is to be extended until 2023, with a regional price cap being introduced from March 2021. However, a lot of people still have questions about exactly what Help to Buy is.

How does it work? Is it right for me? Am I eligible? What is the process? How does the equity loan work?

We will look to answer some of these questions below, along with highlighting the value of an intermediary in guiding you through the entire process.

Who is eligible?

A simple place to start. Help to Buy is available to anyone looking to purchase a property to live in, as long as they will not own any other property, or a share in any other property, at completion of the new purchase.

As such, the scheme has been particularly focused on assisting first-time buyers. However, as long as you sell your existing property before completion, Help to Buy is also available to home movers.

From March 2021 the scheme will only be available for first-time buyers, so home movers wanting to purchase with Help to Buy need to do so before then.

What is Help to Buy and how does the equity loan work?

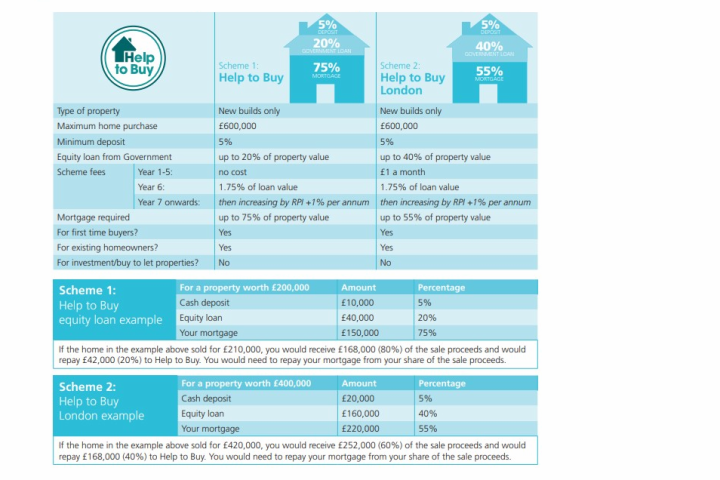

Help to Buy is a government scheme to make home ownership more accessible to both first-time buyers and home movers. It is available to those with a deposit of at least 5%, who are buying a home for a maximum of £600,000. It is only available on new build properties, and these properties must be registered to sell as Help to Buy.

For Help to Buy the government can assist with an equity loan of up to 20% of the purchase price, and with Help to Buy London this increases to 40%. The table below shows some examples of this. The equity loan is interest free for the initial five-year period, after which interest is payable on this element.

The equity loan can either be repaid in full or in part (typically 10% increments of the updated property value). This can be done on the sale of the property, whereby the government will receive their equity share percentage of the sale price, or it can be done via a remortgage.

The purchase of shares of the equity loan, but not to outright ownership, is known as ‘staircasing’. An intermediary with experience in working with the Help to Buy scheme will be able to talk you through these options in detail at your initial meeting.

Is Help to Buy right for me?

It is also important to note that Help to Buy will not be the right choice for everybody. It means having an equity loan on which interest will be payable after five years. It is important to ensure that you are comfortable with the details of the scheme and all of the options and implications for the duration of the mortgage and the equity loan.

What’s the process for the Help to Buy and mortgage applications?

One of the major differences when purchasing using Help to Buy is that there are, in effect, two applications to proceed with.

There is the mortgage application process and also a separate application for Help to Buy. The Help to Buy application process has its own criteria and affordability checks that often differ from those of the mortgage lenders.

As such, it is vital that you speak to an intermediary who understands the Help to Buy scheme and who has access to the Help to Buy affordability calculator. This will allow you to accurately confirm your budget before looking to view any properties.

The good news is that mortgage lenders take the equity loan into account as part of the deposit funds when calculating the rate of interest on the mortgage. This means the mortgage rates tend to be much lower than a typical mortgage with a 5% deposit, with monthly payments regularly lower than clients pay in rent.

As an example, there is currently a two-year fixed rate at just under 1.5% available for a client with a 5% deposit purchasing with Help to Buy, whereas a rate will typically be between 3 to 3.5% for a standard purchase with a 5% deposit. We will show a case study highlighting this later in the article.

The process in brief:

1.To ensure you have an accurate budget for properties to view you need to have your affordability checked with an adviser who will cover the requirements of both the mortgage lender and Help to Buy. You will be able to get the mortgage agreed in principle at this stage.

2.Once you have your budget confirmed and your mortgage agreed in principle you should arrange to view some properties to get a feel for what is available. Most developers will have stock for sale via Help to Buy, and local properties will be listed on the Help to Buy website.

3.Once you put in an offer on a property and have this accepted, the developer will ask you to complete a reservation form. At this stage a non-refundable deposit, typically around £500, is required. You will be given a set amount of time, typically 28 days, in which your mortgage and Help to Buy application must be agreed.

4.At this stage your adviser will submit your applications to the mortgage lender and also your Help to Buy application. (Note: not all intermediaries have access to do this. If your intermediary does not, you will need to submit this application directly to the housing association yourself). The mortgage lender will instruct the valuation on the property when you submit the mortgage application at this stage.

A tip – if the Help to Buy application form includes any incorrect information, it has to be applied for again and you go to the back of the queue. It really is key to get this right first time!

5.Once your documentation is assessed and approved you will receive a mortgage offer from the lender and a document called Authority To Proceed from Help to Buy. Once you have these your solicitor will be able to arrange exchange of contracts on the purchase. This is when all sides are legally committed to the purchase, and a date is set for completion – when you get the keys.

Case study

Let’s take a look at a case study. These recent Alexander Hall clients illustrate how Help to Buy can benefit a first-time buyer perfectly (names have been changed).

The clients:

A young couple, Michael and Emma, are both young first-time buyers. Michael is a manager at a financial services firm and Sarah is a PA on a basic salary.

The scenario:

Michael and Emma were renting for the last few years in central London and met a mortgage adviser to discuss purchasing, but with the budget they were given felt they could not find a property that would match their needs.

The clients had a £35,000 deposit thanks to some savings and a family gift but were advised with their incomes they had a maximum purchase price of £350,000.

The solution:

Michael and Emma saw some properties advertised on the Help to Buy scheme and met one of our advisers to discuss their options. After the calculations were run through with Help to Buy and with the mortgage lenders, a maximum purchase price of £500,000 was achievable.

This meant the clients could purchase a two-bedroom house in their local area, and with monthly payments at less than half of their existing rental payments.

- Property value: £500,000

- Loan amount: £300,000 (and a £175,000 equity loan)

- LTV: 60%

- Rate: 1.54% 2 year fixed

- APRC: 3.7%

- Term: 35 years capital repayment

- Lender arrangement fee: £999 added to loan amount

- Mortgage payment: £930pcm

This article was originally posted in What Mortgage online. You can see the original article here. Please note this will launch a new web page.